- About Us

- Solutions

- Industries

- Case Studies

- Resources

- Contact Us

Sustainable Fuel Resolution: A Global Push for Green Hydrogen Production

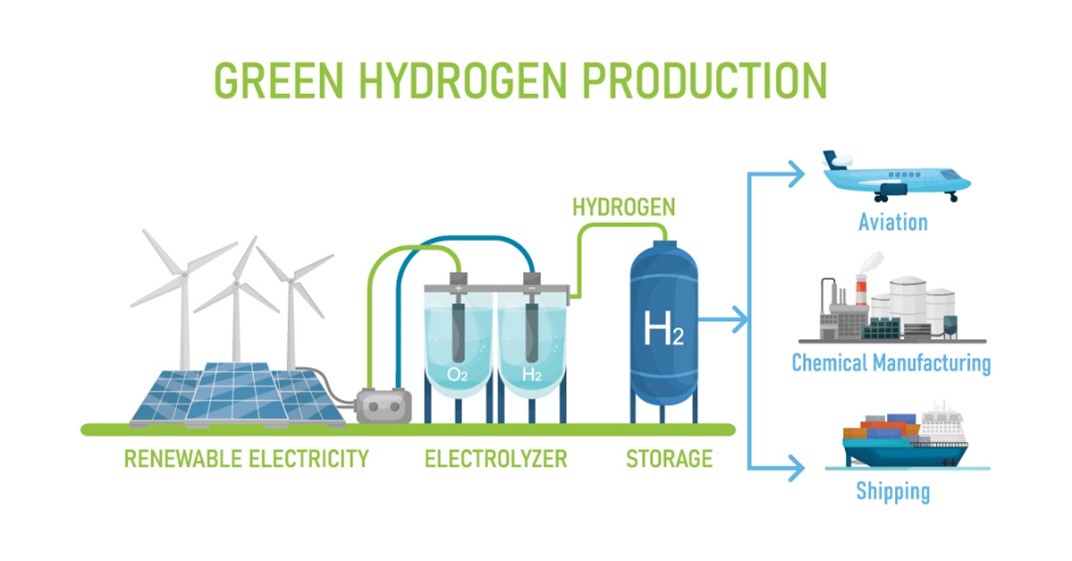

In an attempt to tackle the challenge of climate change, global leadership is actively promoting the research, development, and utilization of alternative sustainable fuels. Currently, green hydrogen, in contrast to other synthetic green fuels, is considered as a key enabler of clean energy transition. It has the exceptional quality of being the sole clean energy molecule that can be produced at any scale and in almost every region on Earth.

Thus, green hydrogen production may enable virtually any organization or country to manufacture its own fuels, with the flexibility for a range of end uses, including usage for oil and gas, industrial feedstock, transportation, and power generation.

Hydrogen serves as an energy carrier in a variety of applications, such as oil and gas, industrial feedstock, transportation, and power generation. However, its current usage is extremely constrained due to its heavy dependency on fossil fuels for the manufacturing process. At the moment, natural gas and coal together make up around 99% of hydrogen output. Only less than 1% of the world's hydrogen is produced by sustainable procedures such as electrolysis, which in turn makes it a green hydrogen fuel.

Currently, the most common ways to produce hydrogen are by gasification and reforming of natural gas, with most of these processes taking place in China. Together, these activities produce between 96% to 99% of the hydrogen used in the world.

Despite the potential of green hydrogen as a next generation fuel alternative, fossil fuels are still used to produce hydrogen today due to their plentiful supply and easy access. Major advancements are required to decarbonize the current process and scale up green hydrogen production globally.

As a result, numerous government programs and policies are being pushed globally to encourage and support green hydrogen production, which is significantly boosting the global market for green hydrogen.

According to the BIS Research report, the global green hydrogen market was valued at $227.7 million in 2021 and is projected to reach $108.64 billion by 2031, registering a CAGR of 68.9% between 2022 and 2031 in terms of value.

Find more details on this report in this FREE sample

Further in the article, crucial government policies that are aiming to push green hydrogen production in the coming years are discussed further in detail.

List of Crucial Policies Impacting the Future of Green Hydrogen Production

In the coming years, a wave of government subsidy programs will go into effect that will essentially guarantee profitability for sustainable green hydrogen fuel projects, which will, in turn, require enormous amounts of clean power to operate. This will turn the widely discussed green hydrogen technology into a large-scale reality.

U.S. Inflation Reduction Act - A Great Boost for Green Hydrogen Production

The Inflation Reduction Act (IRA), which combines a wide range of renewable energy tax incentives into a single law, was passed by the U.S. Congress in the summer of 2022. Over the next ten years, the U.S. government has committed to spending $369 billion under this new law to address energy security and climate change. A valuable package of tax credits that are part of the IRA is essential because they will hasten the adoption of green hydrogen technology and other clean energy sources. Some automakers have also entered the green hydrogen market as a result of this financial backing, with some even planning to expand the production of green hydrogen fuel vehicles and develop new infrastructure.

Due to its potential to decarbonize transportation, including road, aviation, and shipping, green hydrogen fuel created from renewable electricity has received much interest. However, the cost is a key obstacle to its adoption.

The IRA has added additional rules for green hydrogen production and increased tax credits for renewable electricity. According to the act, for the first ten years of operation, 2023 will see production tax credits for green hydrogen technology and renewable power plants of up to $3 per kilogram of hydrogen and 2.6 cents per kWh, respectively (their lifetimes are typically up to 30 years). The tax breaks, however, are only in effect until 2032, meaning that projects beginning in 2023 would receive all of the 10 years' worth of credits, while plants beginning later would receive progressively less.

For green hydrogen fuel manufacturers, the IRA's provisions are beneficial for a number of reasons. First, both tax credits are available to manufacturers of green hydrogen production from renewable electricity. In addition, for the first five years of operation, the hydrogen tax credit is "direct pay," allowing green hydrogen producers to request a tax return equivalent to the amount of their tax credits. Furthermore, tax "transferability,” which is the ability of producers with no tax liability to sell their tax credits to a buyer with tax liability, can be advantageous for both producers of green hydrogen fuel and renewable power.

The IRA is putting out a positive message on the wide adoption of green hydrogen fuel. For plants that utilize the entire set of tax credits going online this year, the tax credits offered in the IRA can reduce the cost of green hydrogen production by half.

The U.S. is still a long way from having a green hydrogen economy, and even with tax credits, green hydrogen technology is not a panacea for all problems. Green hydrogen fuel probably makes the most financial sense for end-user industries that are difficult to directly electrify, such as industrial usage, long-haul aviation, and shipping, due to its high prices and conversion losses.

EU’s Carbon Contracts for Difference Aiming to Subsidise Green Hydrogen Fuel

In May 2022, the European Commission declared that it would use funds from its Innovation Fund to implement Carbon Contracts for Difference (CCfD) subsidies for green hydrogen fuel. This move was made in order to "support a full switch of the existing hydrogen production in industrial processes from natural gas to renewables and the transition to green hydrogen production processes in new industrial sectors such as steel-making."

This is intended to assist in achieving the European Union’s (EU's) goal of producing ten million tonnes of green hydrogen fuel per year within the EU by 2030 and importing an additional ten million tonnes by that time.

Governments would compensate end users (as opposed to producers) with a fixed sum for reducing carbon dioxide (CO2) emissions. The savings from forgoing the payment of a carbon price under the EU's Emissions Trading System (ETS) would be added to a top-up subsidy to bring the "strike price" established in the CCfD to fruition.

Since the amount actually paid by governments would depend on the variable ETS carbon price, if it rose above the strike price, end users would be responsible for paying the difference.

The European Parliament's decision against the European Commission's proposal for hourly verification of dedicated renewable energy supply to electrolyzers caused the publication of the green hydrogen scheme's final details, which were scheduled to be released in 2021, but got postponed.

It was widely anticipated that a new compromise draught proposal, which would allow quarterly matching of dedicated renewable energy supply to green hydrogen production until 2028 before switching to hour-by-hour correlation, would be formally published, but the year ended with no news on the subject.

The 27 member states and the European Parliament would still need to formally approve this proposed regulation, but the European Commission is eager to implement the CCfD program as soon as possible to give the European Union a chance to meet its goal of producing ten million tonnes of green hydrogen fuel annually by 2030.

It is anticipated that the regulations will also apply to green hydrogen imported into the EU. In addition to all of this, the EU-authorized member states will provide subsidies for 3.5 gigawatts (GW) of new electrolysis capacity under the Hy2Use initiative in September 2023.

Germany's H2Global Encouraging Green Hydrogen Technology

The most advanced of all the programs is Germany's multibillion-dollar H2Global green hydrogen subsidy program, which is only available for hydrogen and derivatives imported into the EU. However, manufacturers are not anticipated to receive financing until 2024 at the earliest.

The German government announced two tenders for imported green hydrogen fuel derivatives in December 2022. One contract was for green ammonia, and the other was for green methanol and sustainable aviation fuels based on hydrogen.

A special purpose company owned by the German government by the name of the Hydrogen Intermediary Network Company (HintCo) is set to purchase green hydrogen or its derivatives from international producers via ten-year Hydrogen Purchase Agreements (HPAs) and then sell it to European customers who will bid for short-term supply contracts via separate tenders. This process is known as the unique double-auction scheme used by H2Global.

The best bids will receive the supply contracts, but if their offers fall short of the HPA's price, HintCo will use cash provided by the German government to make up the gap.

H2Global will offer international green hydrogen producers the long-term pricing and demand certainty they want to develop their projects while also assuring a supply for European clients, as the commercial risk will be handled by HintCo.

Olaf Scholz, the German chancellor, has already approved a total of $4.24 billion in funding for H2Global, but the EU has only approved the initial $900 million tranche. The HPA auctions will be finished by the government by the middle of 2023, while the supply auctions will not start until 2024-2025.

U.K.’s CfD Scheme Funding Green Hydrogen Production

The U.K. stated in April 2022 that a Contracts for Difference (CfD) subsidy program for green hydrogen production would be completed by the end of 2022, and in July, it encouraged green hydrogen manufacturers to register "expressions of interest" in the scheme – the first step in the application process.

The government pledged to provide funding for up to 1GW of green hydrogen projects, all of which would be up and running by 2025. This funding would be distributed "through two allocation rounds in 2023 (starting in 2022) and 2024 (starting in 2023)." Around 250MW of projects would be supported in the initial funding round, it was stated.

The CfD program has not been finalized, though, probably as a result of the fact that Britain has had three successive Conservative prime ministers in charge.

The difference between a "strike price," indicating the cost of producing hydrogen, and a "reference price," reflecting the market value of hydrogen, will be represented by the subsidy offered by the hydrogen CfD, according to government explanations provided in April 2022.

In essence, this would make grey hydrogen produced from fossil gas, which is currently burning unchecked, equally expensive to the market as green hydrogen.

Green hydrogen continues to be a top priority for the U.K. government. According to an updated national hydrogen strategy, Westminster intends to "deliver final grant offer letters in early 2023" to selected green hydrogen producers who have submitted expressions of interest.

It was announced in December 2022 that a market engagement exercise on a second funding round for renewable H2 would begin in the second quarter of 2023. As part of its effort to build 5 GW of clean H2 by 2030 and 25 GW by 2045, the Scottish government has also introduced its own $112 million Green Hydrogen Fund and announced that it would launch a "call for proposals" for renewable H2 projects in early 2023.

However, specifics of how the funds would be distributed have not yet been made public.

Conclusion

The development of global "net zero" carbon emission objectives has been one of the most noteworthy characteristics of climate policy, which is expected to favor the growth of the green hydrogen market that will eventually lead to large-scale green hydrogen production. Europe, the U.K., China, South Korea, Japan, Canada, South Africa, and the U.S. have all adopted these objectives with great ambitions.

Interested to know more about the growing technologies in your industry vertical? Get the latest market studies and insights from BIS Research. Connect with us at hello@bisresearch.com to learn and understand more.

Get DeepTech Insights in your Mailbox!

Popular Posts

- Mycelium: A New Age Packaging Material

- Eco-Friendly Fabrics: The Rise of Castor Oil Biopolymers in the Textile Industry

- World’s First Single Piece 3D-Printed Rocket Engine is Ready to Thrust its First Flight

- Precision Optics in the Next Decade: What to Expect and What's Possible

- Satellite Surveillance – How is it Helpful During the COVID-19 Pandemic?

Recent Posts

- What Factors are Accelerating the Heavy-Duty Autonomous Vehicle Market?

- Space-Based Laser Communication Market: Dynamics and Regional Outlook

- Future of Agri-Drones Market Size, Share, Growth, and Forecast

- Cislunar Infrastructure Market Outlook: Trends and Future Prospects

- Solid Oxide Electrolyzer Cell Market Size, Innovation & Outlook

Posts by Topic

- Healthcare & Medical (83)

- Market Research Report (40)

- Agriculture & Food Tech (29)

- Advanced Materials & Chemicals (27)

- Automotive (27)

- Covid-19 (24)

- Aerospace defense (23)

- Robotics & UAV (23)

- Coronavirus (22)

- 3D Printing (20)

- Digital Technology (15)

- Electronics & Semiconductor (15)

- novel covid-19 (14)

- Electronic Cigarette (11)

- Precision Agriculture (11)

- novel coronavirus (10)

- Security & Surveillance (9)

- Artificial Intelligence (8)

- Webinar (8)

- corona virus (8)

- 3D Printing Market (7)

- BIS Research (7)

- precision agriculture market (7)

- BIS Research Webinar (6)

- Blockchain technology (6)

- Building Technologies & HVAC (6)

- Healthcare (6)

- Market Trends (6)

- UAV (6)

- Energy and sustainability (5)

- Waste Management & Envir Tech (5)

- covid19 (5)

- e-cigarette (5)

- electronic cigarette (5)

- precision medicine market (5)

- Agriculture (4)

- Automotive Cybersecurity (4)

- Computed Tomography (4)

- Electric Vehicles (4)

- Precision Farming (4)

- Surgical Procedure Volume Database (4)

- Unmanned Aerial Vehicles (4)

- automotive cybersecurity market (4)

- precision medicine (4)

- precision medicine report (4)

- 3D Printer (3)

- 3D Printing Technology (3)

- Augmented Reality and Virtual Reality Market (3)

- Big Data (3)

- Biomanufacturing 4.0 (3)

- Counter-UAS Technology (3)

- Drones (3)

- EV Batteries (3)

- EV Battery Market (3)

- Healthcare Industry (3)

- Internet of Things (3)

- IoT in Agriculture Market (3)

- Market (3)

- Market Forecast (3)

- Plastics (3)

- Small Modular Reactor Market (3)

- SpaceTech (3)

- Surgical Robotics Market (3)

- bis research blog (3)

- e liquid market forecast (3)

- e-cigarette market (3)

- electronic cigarette market (3)

- healthcare sector (3)

- market research report (3)

- noval corona virus (3)

- precision agriculture industry (3)

- precision agriculture report (3)

- precision farming market (3)

- precision medicine industry (3)

- space and aerospace (3)

- surgical robotics market growth (3)

- telemedicine (3)

- uav market forecast (3)

- 2016-2021 (2)

- 3D Printing Application Market (2)

- 3D Printing Market Analysis (2)

- 3D Printing Material (2)

- 3D Printing Material Market (2)

- 3D Printing Technology Market (2)

- 6G Technology (2)

- ADAS Market (2)

- AI-Enabled Medical Imaging Solutions Market (2)

- Advanced Space Composites Industry (2)

- Advanced Space Composites Market (2)

- Advanced Space Composites Report (2)

- Advanced Wound Dressing Market (2)

- Advancements in Augmented Reality (2)

- Aerospace (2)

- Agricultural Industry (2)

- Agricultural Sensors (2)

- Agriculture & Food (2)

- Agriculture Dealers Industry (2)

- Agriculture Dealers Market (2)

- Agriculture Drones and Robots Market (2)

- Agriculture Industry (2)

- Agriculture IoT (2)

- Agriculture Technology-as-a-Service Market (2)

- Augmented Reality (2)

- Automotive LiDAR Market (2)

- Automotive LiDAR Market Research (2)

- Automotive Market (2)

- Autonomous Vehicle (2)

- Autonomous Vehicle Market (2)

- Autonomous Vehicle Simulation Solutions Market (2)

- BVLOS drones (2)

- Battery (2)

- Blockchain Technology Market (2)

- CAD Market (2)

- CRISPR Technology Market (2)

- CRISPR Technology Market forecast (2)

- CRISPR Technology Market report (2)

- CRISPR Technology Market share (2)

- CRISPR Technology Market trends (2)

- CRISPR Technology Market value (2)

- CRISPR Technology Marketresearch (2)

- Carbon Negative (2)

- Cell and Gene Therapy (2)

- Cognitive Electronic Warfare System (2)

- Commercial Drones (2)

- Commercial Vehicles (2)

- Computed Tomography Industry (2)

- Computed Tomography Market (2)

- Computer Aided Design Market (2)

- Consumer Printer (2)

- Crop Production (2)

- Cybersecurity (2)

- Defense Market (2)

- Diagnostic Imaging Market (2)

- Digital Agriculture Marketplace Market (2)

- Digital Technology Market (2)

- Disposable Protective Apparel (2)

- Drone (2)

- ENT Devices Market (2)

- EV Battery Pack Cooling System Industry (2)

- EV Battery Pack Cooling System Market (2)

- EV Battery Pack Cooling System Market Research (2)

- EV Battery industry (2)

- EV Battery report (2)

- Early Multicancer Detection (2)

- Electric Vehicle Battery industry (2)

- Electric Vehicles Battery Market (2)

- Emerging technology (2)

- Food Safety Testing Market (2)

- Food Safety Testing Services Market (2)

- Fuel Cells Market (2)

- Games of Skill Market (2)

- Global Augmented Reality Market (2)

- Global Augmented Reality and Virtual Reality Marke (2)

- Global Automotive Telematics Market (2)

- Global Automotive Telematics Market Report (2)

- Global Beacons Technology Market (2)

- Global Beacons Technology Market Analysis (2)

- Global Beacons Technology Market Analysis and Fore (2)

- Global Beacons Technology Market Forecast (2)

- Global Beacons Technology Market Research (2)

- Global Beacons Technology Market Share (2)

- Global CRISPR Technology Market (2)

- Global Carbon Nanotube Market Report (2)

- Global Carbon Nanotube Market Trends (2)

- Global Continuous Fiber Composites Market (2)

- Global Drone Market (2)

- Global EV Battery Market (2)

- Global Food Safety Testing Market (2)

- Global Food Safety Testing Market Analysis (2)

- Global Food Safety Testing Market Trends (2)

- Global Food Safety Testing Market growth (2)

- Global Industrial Microbiology industry analysis (2)

- Global Industrial Microbiology industry report (2)

- Global Intelligent Lighting Controls Market (2)

- Global Liquid Biopsy End User Market (2)

- Global Liquid Biopsy Market Share (2)

- Global Markets and Technologies for Food Safety (2)

- Global Medical Image Analytics Market (2)

- Global Next Generation Sequencing (2)

- Global Next Generation Sequencing Market Share (2)

- Global SLAM Technology Market (2)

- Global SLAM Technology Market Size (2)

- Global SLAM Technology Market Size by Country (2)

- Global SLAM Technology Market by Region (2)

- Global SLAM Technology Market for Robot (2)

- Global SLAM Technology Market for Robots by Commer (2)

- Global SLAM Technology Market for Robots by Househ (2)

- Global SLAM Technology Market for UAV (2)

- Global SLAM Technology Market forecast (2)

- Global SLAM Technology Market growth (2)

- Global SLAM Technology Market report (2)

- Global SLAM Technology Market research (2)

- Global SLAM Technology Market share (2)

- Global SLAM Technology Market trends (2)

- Global Surgical Robotics Market (2)

- Global UAV Sense and Avoid Systems Market (2)

- Global UAV market (2)

- Global Video Surveillance Market (2)

- Global iBeacon Market Size (2)

- Global liquid biopsy market (2)

- Global small caliber ammunition market (2)

- HVACR (2)

- HVACR Market (2)

- Healthcare Robots Trends (2)

- Heating Equipment Market (2)

- IOT in Oil and Gas (2)

- IVD Market (2)

- Immersion Cooling Fluids Industry (2)

- Immersion Cooling Fluids Market (2)

- Immersion Cooling Fluids Report (2)

- In-Space Economy (2)

- In-Vitro Fertilization Market (2)

- Indoor Vertical Farming (2)

- Industrial IoT Market (2)

- Industrial Microbiology Market (2)

- Industrial Microbiology Market Report (2)

- Industrial Microbiology Market forecast (2)

- Industrial Microbiology Market share (2)

- Industrial Microbiology Market size (2)

- Industrial Microbiology Market trends (2)

- Industrial microbiology (2)

- IoT (2)

- LED (2)

- LED Market (2)

- LiDAR Market (2)

- Lightweight Rooftop Solar PV Industry (2)

- Lightweight Rooftop Solar PV Market (2)

- Lightweight Rooftop Solar PV Report (2)

- Liquid Biopsy (2)

- Liquid Biopsy Market Size (2)

- Liquid Cooling Industry for Stationary BESS (2)

- Liquid Cooling Market for Stationary BESS (2)

- Liquid Cooling Report for Stationary BESS (2)

- Liquid biopsy market (2)

- Lithium-Ion Batteries (2)

- LoRaWAN (2)

- Low-Carbon Aluminum Industry (2)

- Low-Carbon Aluminum Market (2)

- Low-Carbon Aluminum Report (2)

- Machine learning (2)

- Market Growth (2)

- Medical Imaging Market (2)

- Mental Health (2)

- Microbiome Modulators Market (2)

- NGS Sample Preparation Market (2)

- NIPT (2)

- Nanocoatings Market (2)

- Neurostimulation Devices Market Share (2)

- Neurostimulation Devices Market growth (2)

- Neurostimulation Devices market (2)

- Non-Invasive Prenatal Testing Market (2)

- Powered Agriculture Equipment Market (2)

- Precision medicine market growth (2)

- Precision medicine market report (2)

- Precision medicine market size (2)

- Precision medicine market trends (2)

- Prefilled Syringes Market (2)

- Radiation Dose Management (2)

- Reconfigurable Battery Systems Industry (2)

- Reconfigurable Battery Systems Market (2)

- Reconfigurable Battery Systems Report (2)

- Remote Drone Identification System Market Size (2)

- Robotics and Imaging (2)

- SLAM Technology for Augmented Reality (2)

- SLAM Technology for Autonomous Vehicles (2)

- SLAM Technology for Robots (2)

- SLAM Technology for UAV (2)

- SLV Market (2)

- Satellite Spectrum Monitoring (2)

- Satellite Spectrum Monitoring Market (2)

- Satellites (2)

- Sensor (2)

- Small Launch Vehicle Market (2)

- Small Modular Reactor Industry (2)

- Small Modular Reactor Report (2)

- Small Satellite Market Forecast (2)

- Smart Lighting Market (2)

- Sodium-Ion Battery Industry (2)

- Sodium-Ion Battery Market (2)

- Sodium-Ion Battery Report (2)

- Space-Based Laser Communication Industry (2)

- Space-Based Laser Communication Market (2)

- Space-Based Laser Communication Report (2)

- Surgical Robotics (2)

- Surgical Robotics Market trends (2)

- Surgical Robotics industry (2)

- Surgical Robotics report (2)

- Sustainable Future (2)

- Sustainable Space (2)

- Switchgear Monitoring System Market (2)

- Switchgear Monitoring System Market size (2)

- Tactical UAV Industry (2)

- Tactical UAV Market (2)

- Tactical UAV Report (2)

- UAVs (2)

- UK E cigarette market (2)

- Unmanned Aerial Vehicles Market (2)

- VTOL Aircraft Market (2)

- Vertical Farming (2)

- Wearable Technology (2)

- White Hydrogen Market (2)

- Wound Cleanser Products Market (2)

- advanced electronic materials (2)

- anti money laundering software market size (2)

- applications of crispr technology (2)

- automotive sector (2)

- beacon market research (2)

- beacon market size (2)

- beacon marketing solutions (2)

- beacon technology (2)

- beacon technology market research (2)

- beacon technology market size (2)

- biometric identification market (2)

- bluetooth beacon technology (2)

- cancer treatment (2)

- cannabis market in North America (2)

- corona (2)

- crispr cas technology (2)

- crispr cas9 technology (2)

- crispr gene technology (2)

- crispr news (2)

- crispr technology (2)

- crispr technology companies (2)

- data centers (2)

- data mining (2)

- defense industry (2)

- defense outlook (2)

- drone industry (2)

- drones market research (2)

- drug discovery (2)

- e cigarette market reports (2)

- e liquid market study (2)

- e vapor (2)

- eddystone beacon technology market size (2)

- electric propulsion (2)

- electric vehicle (2)

- electric vehicle industry (2)

- electronic cigarette market report (2)

- european e liquid market (2)

- european e liquid market reports (2)

- fleet management market (2)

- food pathogen testing market size (2)

- food safety market size (2)

- global food safety testing market size (2)

- global healthcare robotics market (2)

- global positioning systems (2)

- green hydrogen technology (2)

- healthcare trends (2)

- high acuity information systems (2)

- hvac market forecast (2)

- hvac market report (2)

- ibeacon for real estate (2)

- iot security market analysis (2)

- iot security market forecast (2)

- liquid biopsy market report (2)

- market size (2)

- medical imaging (2)

- medical robotics industry growth (2)

- micro mobility market (2)

- minimally invasive surgical systems market (2)

- next generation sequencing market (2)

- novel corona virus (2)

- pathogen testing market (2)

- pollution (2)

- robotic surgery market (2)

- robotic surgery market size (2)

- satellite imaging (2)

- small satellite launch market (2)

- space technology (2)

- stratasys (2)

- surgical procedure volume data (2)

- surgical robots market (2)

- uav market report (2)

- unmanned aerial vehicle market (2)

- vape (2)

- vapor (2)

- ventilators (2)

- video surveillance market forecast (2)

- wearable electronics (2)

- what is crispr technology (2)

- world environment day (2)

- 2019 AI Trends (1)

- 3D Cell Culture (1)

- 3D Printed Gown (1)

- 3D Printing Market for Aerospace (1)

- 3D Printing Market for Aerospace Industry by Mater (1)

- 3D Printing Market for Aerospace Industry by Regio (1)

- 3D Printing Market for Automotive (1)

- 3D Printing Market for Automotive Industry by Mate (1)

- 3D Printing Market for Automotive Industry by Regi (1)

- 3D Printing Material Market Forecast (1)

- 3D Printing Materials Market (1)

- 3D Printing Materials Market Research (1)

- 3D Printing Plastic Market (1)

- 3D Printing Plastic and Photopolymer Material Mark (1)

- 3D Printing Software (1)

- 3D Printing Software and Services Market (1)

- 3D Printing Technologies (1)

- 3D Printing Technology Industry (1)

- 3D Printing Technology report (1)

- 3D Printing in Food Industry (1)

- 3D Protein Structure (1)

- 3D printing in Fashion (1)

- 3D printing market report (1)

- 3D printing materials Aerospace (1)

- 3D printing materials Automotive (1)

- 3D printing or additive manufacturing (1)

- 3D printing software market (1)

- 3D printing technology aerospace (1)

- 3D printing technology automotive (1)

- 3D-Printed Rocket Engine (1)

- 3DP (1)

- 3DP Market (1)

- 3DP Meterials Market (1)

- 3DP Technology (1)

- 3d (1)

- 3d Printer in Medical (1)

- 3d bioprinting market (1)

- 3d bioprinting market report (1)

- 3d bioprinting market size (1)

- 3d printed gun (1)

- 3d printing in automotive (1)

- 3d printing in dental (1)

- 3d printing market research (1)

- 3d printing market share (1)

- 3d printing market size (1)

- 3d printing market trends (1)

- 3d printing use case (1)

- 4d printing (1)

- 5G Industry (1)

- 5G Infrastructure (1)

- 5G Infrastructure Industry (1)

- 5G Infrastructure Market (1)

- 5G Infrastructure Market Analysis (1)

- 5G Infrastructure Market By Spectrum Type (1)

- 5G Infrastructure Market Forecast (1)

- 5G Infrastructure Market Growth (1)

- 5G Infrastructure Market Research Report (1)

- 5G Infrastructure Market Share (1)

- 5G Infrastructure Market Trends (1)

- 5G Infrastructure Market by Application (1)

- 5G Infrastructure Market by Region (1)

- 5G Infrastructure Market key[players (1)

- 5G Infrastructure Report (1)

- 5G Market (1)

- 5G Network Industry (1)

- 5G Network Market (1)

- 5G Network Market Study (1)

- 5G Network Report (1)

- 5G Report (1)

- 5G Satellite (1)

- 5G Technology Forecast (1)

- 5G Technology Industry (1)

- 5G Technology Market (1)

- 5G Technology Market Research (1)

- 5G Technology Market Study (1)

- 5G Technology Market Trends (1)

- 5G Technology Report (1)

- 5G Technology Share (1)

- 5G technologies (1)

- 5GNetwork Market Research (1)

- 5g Market Share (1)

- 5g Market Share Analysis (1)

- 5g Market Study (1)

- 5g Market Trends (1)

- 5g market forecast (1)

- ABS (1)

- ADAS (1)

- ADAS Commercial Vehicles Market (1)

- ADAS Commercial Vehicles Market Forecast (1)

- ADAS Market Size by Commercial Vehicles Market (1)

- ADAS Vehicle Market (1)

- ADAS market size (1)

- AGEYE (1)

- AGV (1)

- AGV Market (1)

- AGV Market Analysis (1)

- AGV Market Outlook (1)

- AGV Market Study (1)

- AI Applications (1)

- AI Healthcare (1)

- AI Market Reports (1)

- AI in 2019 (1)

- AI in Healthcare Market (1)

- AI in Healthcare Robotics (1)

- AI in Medical Imaging (1)

- AI in Operating Room Market (1)

- AI in agriculture market (1)

- AI in cybersecurity (1)

- AI systems (1)

- AI-Enabled Medical Imaging (1)

- AI-Enabled Medical Imaging Solutions Industry (1)

- AI-Enabled Medical Imaging Solutions Report (1)

- AI-Powered Cybersecurity (1)

- AI-based ECG technology (1)

- AIP System (1)

- AIP systems for submarines (1)

- AIP technology (1)

- APAC Air Purifier Market (1)

- APAC Air Purifier Market analysis (1)

- APAC Air Purifier Market growth (1)

- APAC Air Purifier Market report (1)

- APAC Air Purifier Market research report (1)

- APAC Air Purifier Market share (1)

- APAC Air Purifier industry analysis (1)

- APAC Air Purifiers Player Share Analysis (1)

- APAC Algae Biofuel Industry (1)

- APAC Algae Biofuel Market (1)

- APAC Algae Biofuel Report (1)

- APAC Autonomous Vehicle Market (1)

- APAC E-cigarette Market (1)

- APAC E-cigarette Market Forecast (1)

- APAC E-cigarette Market Survey (1)

- APAC E-cigarette Market Trends (1)

- APAC E-cigarette Report (1)

- APAC E-liquid Market (1)

- APAC E-liquid Market Forecast (1)

- APAC E-liquid Market Report (1)

- APAC E-liquid Market Size (1)

- APAC E-liquid Market Study (1)

- APAC Fiber Optic Cable Industry (1)

- APAC Fiber Optic Cable Market (1)

- APAC Fiber Optic Cable Report (1)

- APAC HVAC-R Industry (1)

- APAC HVAC-R Market (1)

- APAC HVAC-R Market Report (1)

- APAC Non-Alcoholic Beverage Industry (1)

- APAC Non-Alcoholic Beverage Market (1)

- APAC Non-Alcoholic Beverage Report (1)

- APAC Precision Farming Market (1)

- APAC Space Carbon Composite Fiber Market (1)

- APAC Space Carbon Fiber Composite Industry (1)

- APAC Space Carbon Fiber Composite Report (1)

- APAC TJA Systems Market (1)

- APAC Traffic Jam Assist Systems Market (1)

- APAC microgrid market (1)

- AR (1)

- AR & MR Market Research (1)

- AR Market (1)

- AR and VR Market (1)

- AVping (1)

- Accelermeter (1)

- Acid Metal Complex Dyes Industry (1)

- Acid Metal Complex Dyes Market (1)

- Acid Metal Complex Dyes Report (1)

- Acquistion (1)

- Actuators Market (1)

- Actuators Market Analysis (1)

- Adaptive Lighting Market (1)

- Adaptive Lighting Market Analysis (1)

- Adaptive Lighting Systems (1)

- Added by Bhavya (1)

- Additive manufacturing application market (1)

- Addressable Market Size and Growth Potential (1)

- Adjuvant agriculture (1)

- Advance Energy Storage Market (1)

- Advance Energy Storage Market Trends (1)

- Advanced Dental Digital Solutions Market (1)

- Advanced Dental Robotics Solutions Market (1)

- Advanced Driver Assistance System Market (1)

- Advanced Energy Storage Market Report (1)

- Advanced Energy Storage Market Study (1)

- Advanced Message Queuing Protocol (1)

- Advanced Traffic Management System (1)

- Advanced Transportation Pricing System (1)

- Advanced Traveler Information System (1)

- Advanced Wound Care Market Analysis (1)

- Advanced Wound Care Market Report (1)

- Advanced Wound Care Market Size (1)

- Advanced Wound Care Market Study (1)

- Advanced Wound Care Market Survey (1)

- Advanced Wound Dressing Industry (1)

- Advanced Wound Dressing Report (1)

- Advanced directed energy weapons (1)

- Advanced propane dehydrogenation (1)

- Advances in UAV Communications (1)

- Advancing Precision Medicine (1)

- AeroFarms (1)

- Aeroponics (1)

- Aerospace 3D Printing Industry (1)

- Aerospace 3D Printing Market (1)

- Aerospace 3D Printing Market Forecast (1)

- Aerospace 3D Printing Market Share (1)

- Aerospace 3D Printing Market Trends (1)

- Aerospace 3D Printing Report (1)

- Agnikul Cosmos (1)

- Agri-Drones Market (1)

- AgriDigital (1)

- Agribusinesses (1)

- Agricultural Films Market (1)

- Agricultural Films Market Research Forecast (1)

- Agricultural Films Market Research Report (1)

- Agricultural Films Market Share (1)

- Agricultural Films Market Size (1)

- Agricultural Films Market forecast (1)

- Agricultural Robots Market (1)

- Agricultural Robots Market Analysis (1)

- Agricultural Robots Market Research (1)

- Agricultural Robots Market Trends (1)

- Agricultural Sensors Market (1)

- Agricultural Sprayers Industry (1)

- Agricultural Sprayers Market (1)

- Agricultural Sprayers Report (1)

- Agricultural Tractor Industry (1)

- Agricultural Tractor Market (1)

- Agricultural Tractor Report (1)

- Agricultural adjuvants market (1)

- Agriculture Autonomous Retrofit Industry (1)

- Agriculture Autonomous Retrofit Market (1)

- Agriculture Autonomous Retrofit Report (1)

- Agriculture Autonomous Robots Industry (1)

- Agriculture Autonomous Robots Market (1)

- Agriculture Autonomous Robots Market Report (1)

- Agriculture Autonomous Robots Market Size (1)

- Agriculture Carbon Sequestration Industry (1)

- Agriculture Carbon Sequestration Market (1)

- Agriculture Carbon Sequestration Report (1)

- Agriculture Customer Segmentation Industry (1)

- Agriculture Customer Segmentation Market (1)

- Agriculture Customer Segmentation Report (1)

- Agriculture Dealers Market Report (1)

- Agriculture Dealers Report (1)

- Agriculture Drones (1)

- Agriculture Equipment Industry (1)

- Agriculture Imaging Sensor Industry (1)

- Agriculture Imaging Sensor Market (1)

- Agriculture Imaging Sensor Market Report (1)

- Agriculture Internet of Things Technology Market (1)

- Agriculture Market (1)

- Agriculture Market Report (1)

- Agriculture Sensor Technology (1)

- Agriculture Sensors (1)

- Agriculture Technology-as-a-Service (1)

- Agriculture Tractor Market (1)

- Agriculture technologies (1)

- Agriculture technology (1)

- Agriculture technology Market (1)

- Agrigenomics Market (1)

- Agritech (1)

- Air Cooling (1)

- Air Purifier Market (1)

- Air Purifier Market report (1)

- Airborne LiDAR Services Market (1)

- Airborne LiDAR System Market (1)

- Airborne LiDAR System Market forecast (1)

- Airborne LiDAR System Market gorwth (1)

- Airborne LiDAR System Market report (1)

- Airborne LiDAR System Market scop (1)

- Airborne LiDAR System Market share (1)

- Airborne LiDAR System Market size (1)

- Airborne LiDAR System Market trends (1)

- Airborne LiDAR System Market value (1)

- Aircraft Landing Gear Market Forecast (1)

- Aircraft Landing Gear Market Research (1)

- Algae Biofuel Industry (1)

- Algae Biofuel Market (1)

- Algae Biofuel Report (1)

- Alkaline Water Electrolysis (1)

- Ambulatory Centers (1)

- Ambulatory surgery centers (1)

- America (1)

- America HVACR Market (1)

- America HVACR Market Research (1)

- Americas HVACR Market (1)

- Americas HVACR Market Report (1)

- Americas Heating Ventilation Air Conditioning and (1)

- Americas Prefabricated Steel Building Market Analy (1)

- Ammonia Crackers Industry (1)

- Ammonia Crackers Market (1)

- Ammonia Crackers Report (1)

- Analysis & Forecast (1)

- Analyst brief (1)

- Analysts Note (1)

- Android Auto (1)

- Animal Health Monitoring & Comfort Systems (1)

- Animal genetics (1)

- Anti Fingerprint Industry Analysis (1)

- Anti Fingerprint Market Forecast (1)

- Anti Fingerprint Market Share (1)

- Anti Fingerprint Market Trends (1)

- Anti Fingerprint coatings Industry (1)

- Anti Fingerprint coatings Market (1)

- Anti Fingerprint coatings Report (1)

- Anti Reflective Industry Analysis (1)

- Anti Reflective Market Forecast (1)

- Anti Reflective Market Growth (1)

- Anti Reflective Market Share (1)

- Anti Reflective and Anti Fingerprint Industry (1)

- Anti Reflective and Anti Fingerprint Market (1)

- Anti Reflective and Anti Fingerprint Report (1)

- Anti-Aging Devices Market (1)

- Anti-Aging Devices Market Analysis (1)

- Anti-Aging Devices Market Outlook (1)

- Anti-Aging Devices Market Report (1)

- Anti-Aging Devices Market Share (1)

- Anti-Aging Devices Market Size (1)

- Anti-Aging Devices Market forecast (1)

- Anti-Drone Market (1)

- Anti-Money Laundering Software Market (1)

- Anti-Money Laundering Software market share (1)

- Antibody Conjugate Oligonucleotide market (1)

- Antistatic agents (1)

- Application of Circulating cfDNA (1)

- Aquaponics (1)

- Aquaponics and Hydroponics market forecast (1)

- Aquaponics and Hydroponics market growth (1)

- Aquaponics and Hydroponics market industry analysi (1)

- Aquaponics and Hydroponics market research (1)

- Aquaponics and Hydroponics market share (1)

- Aquaponics and Hydroponics market trend (1)

- Aquaponics and Hydroponics market value (1)

- Aquaponics system market (1)

- Aqueous Zinc Flow Battery Industry (1)

- Aqueous Zinc Flow Battery Market (1)

- Aqueous Zinc Flow Battery Report (1)

- Architecture of Clinical Decision Support System (1)

- Artificial Intelligence Market in Healthcare (1)

- Artificial Intelligence Medical Device Industry (1)

- Artificial Intelligence Medical Device Market (1)

- Artificial Intelligence in Agriculture Industry (1)

- Artificial Intelligence in Agriculture Market (1)

- Artificial Intelligence in Agriculture Report (1)

- Artificial Intelligence in Healthcare (1)

- Artificial Intelligence in Healthcare Robotics (1)

- Artificial Intelligence in Medical Imaging (1)

- Artificial Intelligence in Real Time Monitoring (1)

- Artificial Organs Industry Analysis (1)

- Artificial Organs Market (1)

- Artificial Organs Market Forecast (1)

- Artificial Organs Market Growth (1)

- Artificial Organs Market Report (1)

- Artificial Organs Market Research (1)

- Artificial Organs Market Share (1)

- Artificial Organs Market Trends (1)

- Artificial Organs Market by Organ Type (1)

- Artificial Organs Market by Region (1)

- Artificial Organs Market by Technology (1)

- Artificial Organs industry (1)

- Artificial Organs report (1)

- Artillery (1)

- Aseptic Connectors Market (1)

- Aseptic Pharma Processing (1)

- Aseptic Pharma Processing Market (1)

- Asia Pacific E-cigarette Market (1)

- Asia Pacific E-cigarette Market Research (1)

- Asia Pacific E-cigarette Market Study (1)

- Asia Pacific E-liquid Market Research (1)

- Asia Pacific E-liquid Market Trends (1)

- Asia Pacific Indoor Robots Market (1)

- Asia Pacific Indoor Robots Market Size (1)

- Asia Pacific Livestock Monitoring & Management (1)

- Asia-Pacific Air Purifiers Market (1)

- Asia-Pacific Autonomous Vehicle Market (1)

- Asia-Pacific Cell and Gene Therapy Manufacturing (1)

- Asia-Pacific In-Vitro Fertilization Market (1)

- Asia-Pacific In-Vitro Fertilization Market forecas (1)

- Asia-Pacific In-Vitro Fertilization Market share (1)

- Asia-Pacific In-Vitro Fertilization Market size (1)

- Astrocast’s Sat IoT technology (1)

- Augmented Reality Market (1)

- Auto Injectors Market (1)

- Automated Data Logging Tools and Systems Industry (1)

- Automated Data Logging Tools and Systems Market (1)

- Automated Data Logging Tools and Systems Report (1)

- Automated Guided Vehicle Market (1)

- Automated Guided Vehicle Market Growth (1)

- Automated Guided Vehicle Market Research (1)

- Automated Guided Vehicle Market Trends (1)

- Automated Liquid Handling System Industry (1)

- Automated Liquid Handling System Market (1)

- Automated Liquid Handling System Report (1)

- Automotive 3D Printing Industry (1)

- Automotive 3D Printing Market (1)

- Automotive 3D Printing Market Forecast (1)

- Automotive 3D Printing Market Share (1)

- Automotive 3D Printing Market Trends (1)

- Automotive 3D Printing Report (1)

- Automotive Actuators Market (1)

- Automotive Actuators Market Forecast (1)

- Automotive Actuators Market Research (1)

- Automotive Adaptive Lighting Market (1)

- Automotive Adaptive Lighting Market Research (1)

- Automotive Aftermarket (1)

- Automotive Aftermarket Analysis (1)

- Automotive Aftermarket Research (1)

- Automotive Aftermarket Study (1)

- Automotive Aftermarket Survey (1)

- Automotive Aftermarket Trends (1)

- Automotive Cybersecurity Industry (1)

- Automotive Cybersecurity Report (1)

- Automotive Cybersecurity Threats (1)

- Automotive Fuel Injection Market Forecast (1)

- Automotive Fuel Injection Systems Market Analysis (1)

- Automotive Fuel Injection Systems Market Report (1)

- Automotive Fuel Injection Systems Market Size (1)

- Automotive Fuel Injection Systems Market Trends (1)

- Automotive Infotainment Market (1)

- Automotive Infotainment Systems (1)

- Automotive LiDAR System-on-Chip Industry (1)

- Automotive Lighting Market (1)

- Automotive Lighting Market Forecast (1)

- Automotive Navigation Systems Market forecast (1)

- Automotive Navigation Systems Market growth (1)

- Automotive Navigation Systems Market share (1)

- Automotive Navigation Systems Market trends (1)

- Automotive Power Management IC Industry (1)

- Automotive Power Management IC Market (1)

- Automotive Power Management IC Report (1)

- Automotive Radars Market (1)

- Automotive Refinish Coatings Market (1)

- Automotive Refinish Coatings Market report (1)

- Automotive Refinish Coatings Market research repor (1)

- Automotive Sensors (1)

- Automotive Sensors Industry (1)

- Automotive Sensors Market (1)

- Automotive Sensors Market Research (1)

- Automotive Solid State Battery Industry (1)

- Automotive Solid State Battery Market (1)

- Automotive Solid State Battery Market Forecast (1)

- Automotive Solid State Battery Market Growth (1)

- Automotive Solid State Battery Market Size (1)

- Automotive Solid State Battery Market Trends (1)

- Automotive Solid State Battery Market Value (1)

- Automotive Solid State Battery Market by Component (1)

- Automotive Solid State Battery Report (1)

- Automotive Solid State Battery(SSB) Market (1)

- Automotive Technologies (1)

- Automotive Telematics Market (1)

- Automotive Telematics Market Research (1)

- Automotive Telematics Market Size (1)

- Automotive Telematics Market report (1)

- Automotive Thermoelectric Generator Industry (1)

- Automotive Thermoelectric Generator Market (1)

- Automotive Thermoelectric Generator Market by Comp (1)

- Automotive Thermoelectric Generator Market by Mate (1)

- Automotive Thermoelectric Generator Market by Vehi (1)

- Automotive Thermoelectric Generator Report (1)

- Automotive Trends (1)

- Autonomous Delivery Robots (1)

- Autonomous Driving Components Market (1)

- Autonomous Navigation Software Industry (1)

- Autonomous Navigation Software Market (1)

- Autonomous Navigation Software Report (1)

- Autonomous Vehicle Market Penetration (1)

- Autonomous Vehicle Simulation Industry (1)

- Autonomous Vehicle Simulation Market (1)

- Autonomous Vehicle Simulation Report (1)

- Autonomous Vehicle Simulation Solutions Industry (1)

- Autonomous Vehicle Simulation Solutions Report (1)

- Autonomous cars (1)

- Avoid System Market (1)

- BIS Healthcare (1)

- BIS Research Report (1)

- BTMS (1)

- BVLOS Drone Operations (1)

- Ballasts and LED Drivers Market (1)

- Banking Indoor Robots Market Size (1)

- Battery Manufacturing Equipment (1)

- Battery Manufacturing Scrap Recycling Industry (1)

- Battery Manufacturing Scrap Recycling Market (1)

- Battery Manufacturing Scrap Recycling Report (1)

- Battery Swapping (1)

- Battery Swapping Charging Infrastructure Industry (1)

- Battery Swapping Charging Infrastructure Market (1)

- Battery Swapping Charging Infrastructure Report (1)

- Battery Thermal Management (1)

- Battery Thermal Management System Market (1)

- Beacons Technology for real estate (1)

- Bidirectional EV Charger Market (1)

- Bidirectional EV Charger Report (1)

- Big Data in Healthcare Market forecast (1)

- Big Data in Healthcare Market report (1)

- Big Data in Healthcare Market share (1)

- Big Data in Healthcare Market size (1)

- Big Data in Healthcare Market trends (1)

- Big Data in Healthcare Market value (1)

- Big Data on Healthcare (1)

- Big Tobacco (1)

- Big data analytics (1)

- Big data and IoT (1)

- Binders in Battery Industry (1)

- Binders in Battery Market (1)

- Binders in Battery Report (1)

- Bio-Based Cosmetics (1)

- Bio-Based Green Cosmetics (1)

- Bio-Composite Materials Industry (1)

- Bio-Composite Materials Market (1)

- Bio-Composite Materials Report (1)

- Biodegradable Plastics Industry (1)

- Biodegradable Plastics Market (1)

- Biodegradable Plastics Report (1)

- Bioelectric Medicine Market (1)

- Biofuels Applications (1)

- Biofuels Forecast (1)

- Biofuels Market (1)

- Biofuels Products (1)

- Biofuels Products Market (1)

- Biofuels Report (1)

- Biofuels Technologies (1)

- Biological Role of cfDNA (1)

- Biologics Drug Development (1)

- Biologics Drug Development Industry (1)

- Biologics Drug Development Market (1)

- Biologics Drug Development Market Forecast (1)

- Biologics Drug Development Market Research (1)

- Biologics Drug Development Market Share (1)

- Biologics Drug Development Market Trends (1)

- Biologics Drug Development Report (1)

- Biologics Drug Discovery Market (1)

- Biologics Drug Forecast (1)

- Biologics Drug Industry (1)

- Biologics Drug Market (1)

- Biologics Drug Report (1)

- Biomarkers (1)

- Biomaterials (1)

- Biomaterials Market (1)

- Biomaterials Market Research (1)

- Biomaterials applications (1)

- Biomaterials forecast (1)

- Biomaterials trends (1)

- Biometric Authentication and Identification Indust (1)

- Biometric Authentication and Identification Market (1)

- Biometric Authentication and Identification Report (1)

- Biometric Sensors (1)

- Biometric Video Surveillance Industry (1)

- Biometric Video Surveillance Market (1)

- Biometric Video Surveillance Report (1)

- Biopharmaceuticals (1)

- Bioprinting Market analysis (1)

- Bioprinting Market by Application (1)

- Bioprinting Market by Technology (1)

- Bioprinting Market keyplayer (1)

- Bioprinting Market share (1)

- Bioprinting Market trends (1)

- Bioprinting Market volume (1)

- Biopsy Devices Industry (1)

- Biopsy Devices Market (1)

- Biopsy Devices Report (1)

- Biorational Market (1)

- Biorational Product Market (1)

- Biorational Product Market Analysis (1)

- Biorational Product Market Research (1)

- Biosensors Market analysis (1)

- Biosensors Market forecast (1)

- Biosensors Market growth (1)

- Biosensors Market share (1)

- Blockchain (1)

- Blockchain Technology Market Analysis (1)

- Blockchain Technology in Financial Services Market (1)

- Blockchain in Agriculture and Food Market (1)

- Blockchain in Energy Market (1)

- Blockchain in Genomics (1)

- Blockchain in Genomics Market (1)

- Blockchain in Healthcare (1)

- Blockchain in Healthcare Market forecast (1)

- Blockchain in Healthcare Market report (1)

- Blockchain in Healthcare Market share (1)

- Blockchain in Healthcare Market trends (1)

- Blockchain in Healthcare Market value (1)

- Blockchain in Healthcare Marketresearch (1)

- Bone Scans (1)

- Brain Disease Modalities and Software Market (1)

- Brain Imaging Modalities Market (1)

- Breaking Barriers in Neurology (1)

- Breast Cancer Screening and Diagnostic Industry (1)

- Brute Force Attack (1)

- Building Energy Management System Market (1)

- Building information modeling (1)

- Business Decisions (1)

- Buy Surgical Procedure Volume Database (1)

- By Communication Infrastructure (1)

- C4ISR Market (1)

- C4ISR Systems (1)

- C4ISR Trends (1)

- CAD (1)

- CAD Industry (1)

- CAD Market Forecast (1)

- CAD Market by Application (1)

- CAD Market by Operating System (1)

- CAD Market by Product Type (1)

- CAD Market by Region (1)

- CAD Market by Technology Type (1)

- CAD Report (1)

- CADx (1)

- CADx Cancer Applications (1)

- CADx Imaging Modalities Market (1)

- CADx Mammography Market (1)

- CADx Market (1)

- CAR T-Cell Therapy (1)

- CDR market (1)

- CES 2015 (1)

- CFC industry analysis (1)

- CFC market for aerospace industry (1)

- CFC market report (1)

- CFC market research (1)

- CFC market size (1)

- CGM (1)

- CGM Market (1)

- CNT (1)

- CNT Market (1)

- CNT Market Forecast (1)

- CNT Market Size (1)

- CNT Market Survey (1)

- COVID-19 Treatment (1)

- COVID-19 diagnostic testing market (1)

- COVID-19 on RNA Sequencing Market (1)

- CRISPR Gene Editing (1)

- CRISPR Gene Editing Market (1)

- CT Market (1)

- Caliber Ammunition market (1)

- Caliber Ammunition market analysis (1)

- Caliber Ammunition market report (1)

- Caliber Ammunition market trends (1)

- Caliber ammunition (1)

- Cancer Diagnostics (1)

- Cancer Immunotherapy Industry (1)

- Cancer Immunotherapy Industry Analysis (1)

- Cancer Immunotherapy Market (1)

- Cancer Immunotherapy Market By Product (1)

- Cancer Immunotherapy Market Forecast (1)

- Cancer Immunotherapy Market Share (1)

- Cancer Immunotherapy Market Size (1)

- Cancer Immunotherapy Market Trends (1)

- Cancer Immunotherapy Market by Region (1)

- Cancer Immunotherapy Market by Therapeutic Indicat (1)

- Cancer Immunotherapy Report (1)

- Cancer biomarkers (1)

- Cancer imaging systems market (1)

- Cancer imaging systems market Analysis (1)

- Cancer imaging systems market report (1)

- Cancer imaging systems market size (1)

- Cancer precision medicine market (1)

- CarPlay (1)

- Carbide Market (1)

- Carbon Credits Industry for AFOLU (1)

- Carbon Credits Industry for Agriculture (1)

- Carbon Credits Market for AFOLU (1)

- Carbon Credits Market for Agriculture (1)

- Carbon Credits Report for AFOLU (1)

- Carbon Credits Report for Agriculture (1)

- Carbon Emissions (1)

- Carbon Farming Industry (1)

- Carbon Farming Market (1)

- Carbon Farming Report (1)

- Carbon Nanotube Market (1)

- Carbon Nanotube Market Growth (1)

- Carbon Nanotube Market Research (1)

- Carbon Nanotube Market Study (1)

- Carbon Neutral Data Center Practices (1)

- Carbon Reduction (1)

- Carbon Removal (1)

- Carbon Removal Technologies (1)

- Carbon di-oxide removal (1)

- Cardiac AI Monitoring and Diagnostics Industry (1)

- Cardiac AI Monitoring and Diagnostics Market (1)

- Cardiac AI Monitoring and Diagnostics Report (1)

- Cardiology Medical Image market (1)

- Cardiovascular Implants (1)

- Carrier Screening Market (1)

- Castor Oil Biopolymers (1)

- Cathode Materials Market (1)

- Cathode Materials Market Growth (1)

- Cathode Materials Market Share Analysis (1)

- Cathode Materials Market analysis (1)

- Cathode Materials Market by Region (1)

- Cathode Materials Market forecast (1)

- Cathode Materials Market trends (1)

- Cell Analysis Industry (1)

- Cell Analysis Market (1)

- Cell Analysis report (1)

- Cell Free DNA Isolation and Extraction Market fore (1)

- Cell Free DNA Isolation and Extraction Market grow (1)

- Cell Free DNA Isolation and Extraction Market repo (1)

- Cell Free DNA Isolation and Extraction Market shar (1)

- Cell Free DNA Isolation and Extraction Market size (1)

- Cell Free DNA Isolation and Extraction Market tren (1)

- Cell and Gene Therapy Development (1)

- Cell and Gene Therapy Manufacturing (1)

- Ceramics (1)

- Chemotherapy (1)

- Chimeric antigen receptor (1)

- China Wire and Cable Industry (1)

- China Wire and Cable Market (1)

- China Wire and Cable Report (1)

- Circular Economy (1)

- Circular Economy Webinar (1)

- Cislunar Infrastructure Industry (1)

- Cislunar Infrastructure Market (1)

- Cislunar Infrastructure Report (1)

- Cleaning Robot Market Size (1)

- Climate Smart Agriculture Industry (1)

- Climate Smart Agriculture Market (1)

- Climate Smart Agriculture Market Report (1)

- Climate Smart Agriculture Market Size (1)

- Clinical Decision Support System (1)

- Clinical Genomics Market (1)

- Clinical decision support systems (1)

- Cloud based Global Clinical Decision Support Syste (1)

- Coalition for the Advancement of Precision Agricul (1)

- Coaxial Cable Industry (1)

- Coaxial Cable Market (1)

- Coaxial Cable Report (1)

- Cobots (1)

- Cochlear Implants Industry (1)

- Cochlear Implants Market (1)

- Cochlear Implants Report (1)

- Cognitive Robotic Process Automation Market (1)

- Cognitive Robotic Process Automation for Finance a (1)

- Cognitive Robotic Process Automation for Insurance (1)

- Cognitive Robotic Process Automation for Telecom a (1)

- Collaborative Robot Hardware Market Analysis (1)

- Collaborative Robot Hardware Market Forecast (1)

- Collaborative Robot Hardware Market Report (1)

- Collaborative Robot Hardware Market Research (1)

- Collaborative Robot Hardware Market Research Repor (1)

- ColorJet Printing (1)

- Colorectal Cancer Test (1)

- Combine Harvesters Industry (1)

- Combine Harvesters Report (1)

- Commercial Aircraft Landing Gear Market Report (1)

- Commercial Aircraft Landing Gear Market Study (1)

- Commercial Drone Camera Market (1)

- Commercial Drone Camera Market Size (1)

- Commercial Drone Camera Market Volume (1)

- Commercial Lighting as a Service Market (1)

- Commercial UAS Markem (1)

- Commercial UAV Market (1)

- Commercial UAV Market Share (1)

- Commercial Vehicle ADAS Market (1)

- Commercial Vehicle ADAS Market Research (1)

- Commercial Vehicle Market (1)

- Commercial Vehicles Market (1)

- Compatibility of 5G Networks (1)

- Compression Bandages Industry (1)

- Compression Bandages Market (1)

- Compression Bandages Report (1)

- Computed Tomography Market Report (1)

- Computed Tomography Report (1)

- Computed Tomography Scans (1)

- Computer Aided Design (CAD) Market (1)

- Computer Aided Design Forecast (1)

- Computer Aided Design Growth (1)

- Computer Aided Design Industry (1)

- Computer Aided Design Industry Analysis (1)

- Computer Aided Design Market Research (1)

- Computer Aided Design Market Share (1)

- Computer Aided Design Report (1)

- Computer Aided Design Trends (1)

- Computer Aided Diagnostics (1)

- Computer Aided Diagnostics Market (1)

- Computer Aided Diagnostics Market Report (1)

- Computer Vision Technology Market for Agriculture (1)

- Constrained Application Protocol (1)

- Constrained Peptide Drugs (1)

- Constrained peptides (1)

- Construction Materials Market (1)

- Construction Sealants Market Report (1)

- Construction Sealants Market share (1)

- Construction Sustainable Materials Market (1)

- Consumer Electronics Show (1)

- Contact Layer Dressings Market (1)

- Continuous Fiber Composites Market analysis (1)

- Continuous Fiber Composites Market forecast (1)

- Continuous Fiber Composites Market growth (1)

- Continuous Fiber Composites Market report (1)

- Continuous Fiber Composites research (1)

- Continuous Fiber Composites trends (1)

- Continuous Glucose Monitoring System Market (1)

- Convertible Telepresence Robot Industry (1)

- Convertible Telepresence Robot Market (1)

- Convertible Telepresence Robot Report (1)

- Core Materials Industry (1)

- Core Materials Market (1)

- Core Materials Report (1)

- Coronavirus disease (1)

- Cost-effective Livestock Monitoring (1)

- Counter-UAV Industry (1)

- Counter-UAV Market (1)

- Counter-UAV Report (1)

- Crickets (1)

- Croatia (1)

- Cultured Meat Industry (1)

- Cultured Meat Market (1)

- Cultured Meat Report (1)

- Cyber Security Market (1)

- Cyber Security Market Research (1)

- Cybercriminals (1)

- Cybersecurity Trends (1)

- DAC Market (1)

- DNA Methylation Detection Technology Market (1)

- DNA/RNA Sample Extraction and Isolation Market (1)

- DNARNA Sample Extraction and Isolation Market (1)

- DRAM DIMM Industry (1)

- DRAM DIMM Market, (1)

- DRAM DIMM Report (1)

- DTC wellness (1)

- DTC wellness products (1)

- Data Center Power Infrastructure Market (1)

- Data Center Refrigerant Market (1)

- Data Center Solution (1)

- Data Management in Agriculture (1)

- Data Mining Software Solutions (1)

- Data Mining Software Solutions Market (1)

- Data Mining Software Solutions Market Report (1)

- Data and Services Market (1)

- Data on Fermented Foods (1)

- Decentralize Agriculture (1)

- DeepTechTalk (1)

- Defense Outlook Report (1)

- Dental Digital and Robotics Solutions Market (1)

- Dental Implants (1)

- Dental Implants Industry (1)

- Dental Implants Market (1)

- Dental Implants Report (1)

- Dental Infections Control Industry (1)

- Dental Infections Control Market (1)

- Dental Infections Control Market Report (1)

- Dental Medical Image Analytics Market (1)

- Dental Radiography (1)

- Dental Radiography Market (1)

- Dental Robotics Solutions Market (1)

- Dental radiographs (1)

- Desktop 3D Printer Market (1)

- Desktop 3D Printer Market Forecast (1)

- Desktop 3D Printer Market Research (1)

- Diagnostic Centers Medical Image market (1)

- Diagnostic Imaging Systems Market (1)

- Digital Breast Tomosynthesis Industry (1)

- Digital Breast Tomosynthesis Market (1)

- Digital Breast Tomosynthesis Report (1)

- Digital Diagnostics Industry (1)

- Digital Diagnostics Market (1)

- Digital Diagnostics Report (1)

- Digital Farm (1)

- Digital Forensic Technology (1)

- Digital Manufacturing (1)

- Digital PCR (1)

- Digital PCR technology (1)

- Digital Technologies (1)

- Digital health (1)

- Direct Air Capture Industry (1)

- Direct Air Capture Market (1)

- Direct Air Capture Report (1)

- Direct-to-Customer Wellness (1)

- Directed Energy Weapons (1)

- Drip Irrigation (1)

- Drone Application Map Tool Industry (1)

- Drone Application Map Tool Market (1)

- Drone Application Map Tool Report (1)

- Drone Camera Market (1)

- Drone Camera Market forecast (1)

- Drone Camera Market share (1)

- Drone Camera Market trends (1)

- Drone Webinar (1)

- Drones In Agriculture (1)

- Drones for Earth Observation (1)

- Drug Infusion Systems Market analysis (1)

- Drug Infusion Systems Market forecast (1)

- Drug Infusion Systems Market growth (1)

- Drug Infusion Systems Market share (1)

- Drug Infusion Systems Market trends (1)

- Drug Infusion Systems industry analysis (1)

- Drug Infusion Systems industry report (1)

- Drug Infusion Systems market value (1)

- Dry X-Ray Films (1)

- E cig (1)

- E cigarette ban (1)

- E cigarette market trend 2015 (1)

- E cigarette survey (1)

- E-cigarette Aftermarket Report (1)

- E-cigarette Vape Shop Aftermarket Trends (1)

- E-cigarette Vape Shop Market Study (1)

- E-liquid (1)

- E-liquid Market (1)

- E-liquid Market Analysis (1)

- E-liquid Market Research (1)

- E-liquid Report (1)

- ECG (1)

- ECG analysis (1)

- ECG monitoring (1)

- EED (1)

- EED Market (1)

- EED Market Growth (1)

- EED Market Size (1)

- EED Report (1)

- EU Green Deal (1)

- EU Green Deal 2050 (1)

- EV Business (1)

- EV Charging (1)

- EV Charging Infrastructure (1)

- EV Charging Management Software Platform Industry (1)

- EV Charging Management Software Platform Market (1)

- EV Charging Management Software Platform Report (1)

- EV Ecosystem (1)

- EV Shock Testing (1)

- EV Testing (1)

- EV Webinar (1)

- EV battery (1)

- EV efficiency (1)

- EV fast charging system market (1)

- EV market (1)

- Earth Observation Satellite (1)

- Earth Observation Satellites (1)

- Earth Observation Satellites Data and Services Mar (1)

- Earth observation (1)

- Earth observation drones market (1)

- Edge Analytics Market analysis (1)

- Edge Analytics Market forecast (1)

- Edge Analytics Market growth (1)

- Edge Analytics Market research report (1)

- Edge Data Center Market (1)

- Electric ATV and UTV (1)

- Electric ATV, UTV, and Golf Cart Industry (1)

- Electric ATV, UTV, and Golf Cart Market (1)

- Electric ATV, UTV, and Golf Cart Market Analysis (1)

- Electric ATV, UTV, and Golf Cart Market Research (1)

- Electric Caravans (1)

- Electric Farm Tractors Industry (1)

- Electric Farm Tractors Market (1)

- Electric Farm Tractors Market Report (1)

- Electric Farm Tractors Market Research (1)

- Electric Farm Tractors Market Size (1)

- Electric Stimulation Sensors (1)

- Electric Vehicle (EV) Battery Housing Market (1)

- Electric Vehicle Battery (1)

- Electric Vehicle Battery Cost Forecast (1)

- Electric Vehicle Battery market (1)

- Electric Vehicle Battery report (1)

- Electric Vehicle Bearings (1)

- Electric Vehicle Ecosystem (1)

- Electric Vehicle Fast Charging System Market Size (1)

- Electric Vehicle Sensor Industry (1)

- Electric Vehicle Sensor Market (1)

- Electric Vehicle Sensor Report (1)

- Electric Vehicle Virtual Prototyping (1)

- Electric Vehicle Virtual Prototyping Market (1)

- Electric Vehicle batteries (1)

- Electric Vehicles Battery Market analysis (1)

- Electric Vehicles Battery Market forecast (1)

- Electric Vehicles Battery Market growth (1)

- Electric Vehicles Battery Market share (1)

- Electric Vehicles Battery Market trends (1)

- Electric Vehicles Battery industry (1)

- Electric Vehicles Battery report (1)

- Electric Vehicles Forecast (1)

- Electric Vehicles Market (1)

- Electric Vehicles Market Research (1)

- Electric Vehicles Market Share (1)

- Electric Vehicles Market Trends (1)

- Electric and Hybrid Aircraft (1)

- Electrochemical Biosensor Technology (1)

- Electromagnetic waves (1)

- Electronic cigarette Market Analysis (1)

- Electronic cigarette Market Size (1)

- Electrophysiology Industry (1)

- Electrophysiology Market (1)

- Electrophysiology Report (1)

- Electrosurgical Devices Market (1)

- Electrosurgical Devices Market analysis (1)

- Electrosurgical Devices Market forecast (1)

- Electrosurgical Devices Market growth (1)

- Electrosurgical Devices Market keyplayer (1)

- Electrosurgical Devices Market report (1)

- Electrosurgical Devices Market trend (1)

- Electrosurgical Devices Market value (1)

- Electrosurgical Devices industry analysis (1)

- Emerging Mental Health, (1)

- Emerging Technologies (1)

- Emerging Trends inIoT in Oil and Gas Market (1)

- Endoscopy Procedure Volume Database (1)

- Endoscopy Procedure for SPDV (1)

- Energy (1)

- Energy Efficient Devices Market (1)

- Energy Efficient Devices Market Analysis (1)

- Energy Efficient Devices Market Study (1)

- Energy Efficient Glass Market (1)

- Energy Efficient Glass Market Forecast (1)

- Energy Efficient Glass Market Research (1)

- Energy Efficient Glass Market Trends (1)

- Energy Efficient Market (1)

- Energy Efficient Market Forecast (1)

- Energy Efficient Market Survey (1)

- Energy Sector (1)

- Energy Storage Market Forecast (1)

- Energy Storage Market Research (1)

- Energy Storage Market Size (1)

- Energy Storage Materials Industry (1)

- Energy Storage Materials Market (1)

- Energy Storage Materials Report (1)

- Enhanced Geothermal Systems Market (1)

- Enhanced Treatment Planning (1)

- Entertainment Robots Market Size (1)

- Environmental sustainability (1)

- Epigenetics Market (1)

- Europe Alternative Cathode Material Industry (1)

- Europe Alternative Cathode Material Market (1)

- Europe Alternative Cathode Material Report (1)

- Europe E-cigarette Aftermarket Forecast (1)

- Europe E-cigarette Aftermarket Research (1)

- Europe E-cigarette Vape Shop Market Analysis (1)

- Europe Electric Vehicle Aftermarket Industry (1)

- Europe Electric Vehicle Aftermarket Market (1)

- Europe Electric Vehicle Aftermarket Report (1)

- Europe Electric Vehicle Insulation Industry (1)

- Europe Electric Vehicle Insulation Market (1)

- Europe Electric Vehicle Insulation Report (1)

- Europe Green Hydrogen Industry (1)

- Europe Green Hydrogen Market (1)

- Europe Green Hydrogen Report (1)

- Europe Heavy-Duty Trailer Industry (1)

- Europe Heavy-Duty Trailer Market (1)

- Europe Heavy-Duty Trailer Report (1)

- Europe Livestock Monitoring & Management Marke (1)

- Europe Marine Biofuel Industry (1)

- Europe Marine Biofuel Market (1)

- Europe Marine Biofuel Report (1)

- Europe Maritime Satellite Industry (1)

- Europe Maritime Satellite Market (1)

- Europe Maritime Satellite Report (1)

- Europe Multiple-Element Gas Container Industry (1)

- Europe Multiple-Element Gas Container Market (1)

- Europe Multiple-Element Gas Container Report (1)

- Europe Non-Alcoholic Beverage Industry (1)

- Europe Non-Alcoholic Beverage Market (1)

- Europe Non-Alcoholic Beverage Report (1)

- Europe RNAi Pesticides Industry (1)

- Europe RNAi Pesticides Market (1)

- Europe RNAi Pesticides Report (1)

- Europe Rocket Upper Stage Engine Industry (1)

- Europe Rocket Upper Stage Engine Market (1)

- Europe Rocket Upper Stage Engine Report (1)

- Europe SOEC Market (1)

- Europe Solid Oxide Electrolyzer Cell Industry (1)

- Europe Solid Oxide Electrolyzer Cell Market (1)

- Europe Solid Oxide Electrolyzer Cell Report (1)

- Europe Sustainable Steel Market (1)

- Europe TJA Systems Market (1)

- Europe Traffic Jam Assist Systems Market (1)

- Europe Waste-to-Hydrogen Industry (1)

- Europe Waste-to-Hydrogen Market (1)

- Europe Waste-to-Hydrogen Report (1)

- Europe automated sample preparation market (1)

- European Indoor Robots Market Size (1)

- European Union Green Deal (1)

- European Union Green Deal 2050 (1)

- Exoskeletons Market Analysis (1)

- Extraction of Circulating cfDNA (1)

- Eye Based Biometric Recognition Systems (1)

- FAA Remote ID (1)

- FHIR system (1)

- FIFA World Cup 2022 (1)

- FIFA World Cup Blog (1)

- Facial-Based Biometric Recognition Systems (1)

- Far-Field Wireless Charging (1)

- Farm Automation (1)

- Farm ERP Industry (1)

- Farm ERP Market (1)

- Farm ERP Report (1)

- Farm Equipment Industry (1)

- Farm Equipment Market (1)

- Farm Equipment Report (1)

- Farm Management Software & Services Market (1)

- Farm management systems (1)

- Farming Techniques (1)

- Fatal Digestive Disorders (1)

- Federal Aviation Administration (1)

- Fermented Feed Ingredient Market (1)

- Fermented Food & Ingredients Market (1)

- Fermented Food and Ingredients Market Research (1)

- Fermented Foods Forecast (1)

- Fermented Foods Industry (1)

- Fermented Foods Ingredients Market (1)

- Fermented Foods Market (1)

- Fermented Foods Trends (1)

- Fiber Composites Market share (1)

- Fibromyalgia Market (1)

- Fibromyalgia Market Outlook (1)

- FinFET Technology Market Growth (1)

- FinFET Technology Market Outlook (1)

- FinFET Technology Market Research Report (1)

- FinFET Technology Market Size (1)

- FinFET Technology Market Study (1)

- FinFET Technology Market Survey (1)

- FinFET Technology Market Trends (1)

- Fixed Biometric Systems (1)

- Fixed Wing Hybrid VTOL Market (1)

- Fixed Wing VTOL Aircraft Market (1)

- Fixed Wing VTOL Aircraft Market Research (1)

- Flame retardants (1)

- Flexible Heaters (1)

- Flexible printed electronic materials (1)

- Floating Data Center Market (1)

- Fluids (1)

- Food Industry (1)

- Food Manufacturing (1)

- Food Safety Testing System Market forecast (1)

- Food Safety Testing System Market research report (1)

- Food Safety Testing System Market share (1)

- Food Safety Testing System Market trends (1)

- Food Safety Testing System industry analysis (1)

- Food Security (1)

- Food Tech Market (1)

- Food Tech Market Forecast (1)

- Food Tech Market Research (1)

- Food Technology (1)

- Food Traceability Market (1)

- Food Traceability Market Forecast (1)

- Food Traceability Market Research (1)

- Food and beverages (1)

- Forensic Technologies (1)

- Forensic Technology Market (1)

- Forensic Technology Market Research (1)

- Forensic Technology Market Trends (1)

- Fuel Cell (1)

- Fuel Cell Market Report (1)

- Fuel Cell Technology (1)

- Fuel Cell Technology Market (1)

- Fuel Injection Market Research (1)

- Fuel Injection Market Study (1)

- Fuel Injection Systems Market Survey (1)

- Full Spectrum LED Grow Lights (1)

- Future of Agri-Drones Industry (1)

- Future of Agri-Drones Market (1)

- Future of Agri-Drones Report (1)

- Future of Green Energy (1)

- GERD Drugs and Devices Market (1)

- GERD Drugs and Devices Market Size (1)

- GERD Drugs market (1)

- GERD Market (1)

- GERD Market Study (1)

- GERD Therapy market (1)

- GERD Therapy market Survey (1)

- GIS-based solutions (1)

- GNSS (1)

- GPS (1)

- GPS in Farming (1)

- GRED (1)

- Gallium Nitride (1)

- Gallium Nitride Market (1)

- Games of Skill Market Analysis (1)

- Gaming Market (1)

- Gastro Intestinal Surgical Procedure Volume Data (1)

- Gastroenterology Procedure (1)

- Gastroesophageal Reflux Disease Drug And Devices M (1)

- Gastroesophageal Reflux Disease Drug Market (1)

- Gastrointestinal Procedure Volumes (1)

- Gastrointestinal Surgical Procedure (1)

- Geely (1)

- Generative AI Market (1)

- Generative AI Market analysis (1)

- Generative AI Market report (1)

- Generative AI Market size (1)

- Genetic Disorders (1)

- Genetic Testing (1)

- Geospatial Imagery Analytics (1)

- Geospatial Imagery Analytics Industry (1)

- Geospatial Imagery Analytics Market (1)

- Geospatial Imagery Analytics Report (1)

- Germany Wire and Cable Industry (1)

- Germany Wire and Cable Market (1)

- Germany Wire and Cable Report (1)

- Glass Prefilled Syringes Market (1)

- Global 3D Printing Material Market (1)

- Global 3D Printing Materials Market (1)

- Global 3D Printing Materials Market Report (1)

- Global 3D Printing Plastic Market (1)

- Global 3D Printing Plastic Market Analysis (1)

- Global 3D Printing Plastic and Photopolymer Materi (1)

- Global 3D Printing Services Market (1)

- Global 3D Printing Software (1)

- Global 3D Printing Software & Services Market (1)

- Global 3D Printing Software Market (1)

- Global 3D printers industry analysis (1)

- Global 3D printers market forecast (1)

- Global 3D printers market size (1)

- Global 3D printers market trends (1)

- Global 3DP Market (1)

- Global 3DP Market Forecast (1)

- Global ADAS Commercial Vehicles Market (1)

- Global ADAS Commercial Vehicles Market Analysis (1)

- Global ADAS for Commercial Vehicles Market (1)

- Global AGV Market (1)

- Global AGV Market Size (1)

- Global AR Market (1)

- Global AR and VR Market (1)

- Global AR and VR Market Research (1)

- Global Advance Energy Storage and Fuel Cell Market (1)

- Global Advanced Driver Assistance System Market (1)